Financial Health and the Intensive Margin of Trade

One sentence summary: Finance facilitates trade for big-sized and productive firms in emerging markets.

The corresponding paper by Deniz Baglan and Hakan Yilmazkuday has been accepted for publication at Emerging Markets Finance and Trade.

Abstract

Using data on 2380 firms from nine emerging countries, this

paper shows that there is a positive and significant relationship between

financial health and the intensive margin of trade. The magnitude of this

positive relationship is shown to depend on several firm characteristics, where

the effects of financial health on firm-level exports are larger for firms with

higher levels of export, bigger size (measured by assets), higher productivity

(measured by value added per worker), and moderate levels of financial health

(measured by cash flow over total assets). The results are robust to the

consideration of foreign ownership and country characteristics as well as

industry and time fixed effects.

Non-technical Summary

International exporting at the firm level is subject to

fixed costs, especially the costs related to finance; e.g., up to 90% of world

trade has been estimated to rely on some form of trade finance. However,

whether these costs are paid for one time (e.g., sunk costs at the time of

entry into international markets) or each time (i.e., financial costs paid any

time exported, such as costs of shipping, duties and freight insurance before

export revenues are realized) is a subject of debate. While the former is

connected to the role of finance in the extensive margin of trade, the latter

is associated with the role of finance in the intensive margin of trade. The

existing literature agree upon the role of finance on the extensive margin of

trade. However, evidence for the role of finance on the intensive margin of

trade is limited.

Within this picture, this paper investigates the relationship

between financial health and the intensive margin of trade. Since financially

more vulnerable firms may have alternative necessities for finance, we also consider

possible nonlinearities arising from the determinants of financial

vulnerability, such as size, productivity and foreign ownership, by employing

parametric threshold and nonparametric estimation models. The Enterprise

Surveys of the World Bank are used, where the data include observations from

2380 firms across nine emerging countries. Exports are measured in U.S. dollars,

financial health is measured by the lagged value of cash flow over total

assets, size is measured by the lagged value of log assets measured in U.S.

dollars, and productivity is measured by the lagged ratio of value added

(measured in U.S. dollars) over the number of workers, where using lagged

values on the right hand side is important to control for any potential

endogeneity problem.

The empirical results show that financial health is a

significant factor in explaining the intensive margin of trade for many firms

in our sample, although the magnitude of the effect changes across firms. When

we search for a systematic explanation, we show that there are significant

nonlinearities in the relationship between finance and the level of exports:

financial health leads to higher levels of exports for highly-exporting, large,

productive or domestically owned firms, after controlling for all else.

Therefore, the role of finance on the intensive margin of trade is subject to

nonlinearities in explanatory variables as suggested by the theoretical

literature (which is discussed in details in the next section).

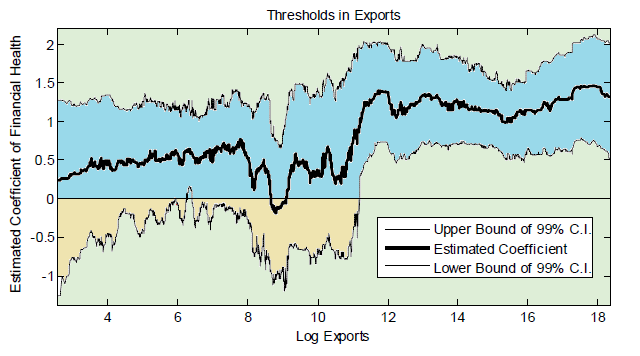

When we search for specific firm characteristics that are

consistent with financial health being effective on the level of exports, we

find through parametric threshold analyses that financial health is positively

and statistically significant more for firms with sizes (measured by assets)

higher than about 1,794,075(=exp(14.4)) U.S. dollars, with productivities

higher than 8.05 U.S. dollars of value added per worker, and with cash flow

over total asset measures more than 0.15. Despite their nonlinear structure,

since parametric threshold models are still restrictive due to their piecewise

linear structure on the financial health function, for robustness, when we

continue our investigation using a nonparametric model, we show that the

results are qualitatively the same and quantitatively very similar to the

parametric threshold analysis. In particular, financial health is positively

and statistically significant mostly for firms with median export values higher

than about 80,000(=exp(11.3)) U.S. dollars (corresponding to about 33% of the

observations in our sample), with median sizes (measured by assets) higher than

about 180,000(=exp(12.1)) U.S. dollars (corresponding to about 50% of the

observations in our sample), with median productivities higher than 7.12 U.S.

dollars of value added per worker (corresponding to about 46% of the

observations in our sample), and with median cash flow over total asset

measures between 0.04 and 1.02 (corresponding to about 68% of the observations

in our sample).

Hence, we provide clues for policy makers regarding which

firms are more beneficial to subsidize in order to achieve higher export

volumes that would support an export-oriented growth strategy. These results

are robust to the consideration of the nationality of firms and

country-industry-time fixed effects which are important to control for the

effects of finance across emerging countries with potentially heterogenous

characteristics where banks may be different or some firms may have export

promotion agencies whilst others may not.